We have heard a lot about contributing to Employees Provident Fund (EPF) – a compulsory retirement fund for those employed set up by our Malaysian government, whereby employers will deduct a percentage of 7%-11% from employees’ salary while contributing additional part of 12%-19% to this retirement fund as a benefit to their employees. As the name suggest, this is a fund for the employees. So how about the employers, the bosses or those self-employed like entrepreneurs and freelancers?

EPF i-Saraan Retirement Scheme

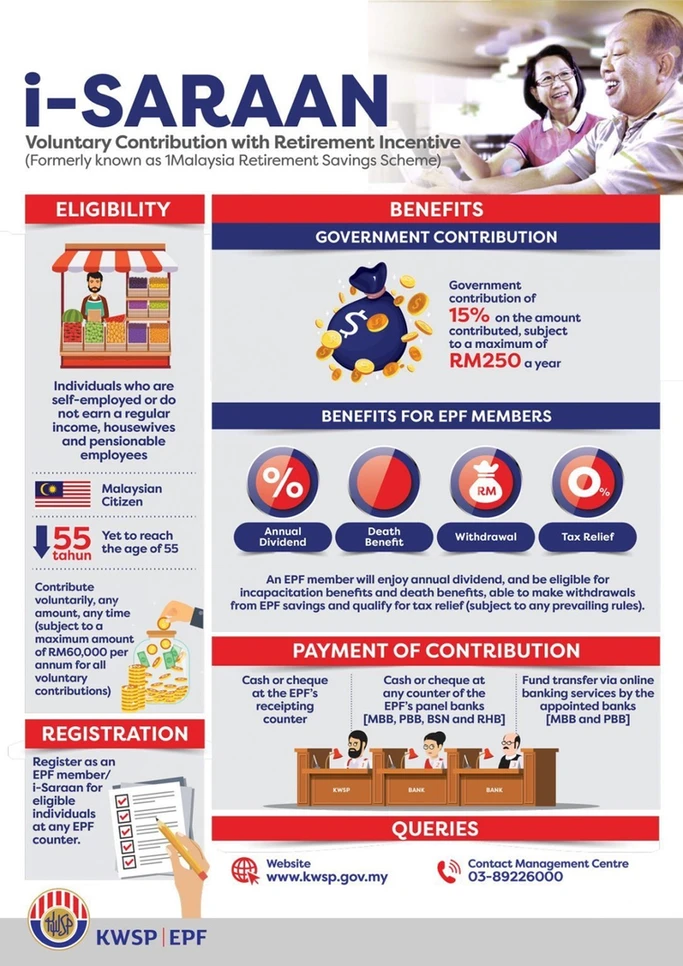

As part of our government’s effort to encourage more people to save money for retirement, EPF has introduced the i-Saraan retirement scheme since 1 January 2018 mainly for the self-employed. Other than the minimum guaranteed return of 2.5% for contributors as given under Section 27 of the EPF Act 1991, another goods news is that the government will match up to 15% (up to maximum of RM250) of the amount contributed by those under this i-Saraan retirement scheme.

Eligibility for i-Saraan

- Self-employed individuals without other employment and those without regular income like housewives*, baby-sitters, freelancers, online business owners, hawkers, farmers, pensionable employees.

- Malaysian citizen below 55 years old

*Housewife is entitled to only one incentive offered by EPF at any time. If she is already registered under the i-Suri incentive, then she can only apply for this i-Saraan retirement scheme if she cancels the i-Suri incentive.

How to Apply

Obtain and complete the Form KWSP 16G(M) which can be found from EPF website and submit it to EPF Officer either over the counter or by mail.

i-Saraan Benefits

- Minimum guaranteed return of 2.5% per annum

- EPF Dividend given until 100 years old

- EPF death benefit of RM2,500

- EPF tax exemption of up to RM4,000

- Government’s matching contribution of 15% (up to maximum of RM250) per annum for 2018-2022

- Can contribute at anytime based on individual’s financial capability with maximum amount of RM60,000 annually

Can I Withdraw Money from EPF Account?

There will be 2 EPF accounts for you once you become a member and start contributing.

- EPF Account 1 (70% of your contribution) – Can withdraw when you reach 55 years old

- EPF Account 2 (30% of your contribution) – Can withdraw before you reach 55 years old for purchase or construction of residential house provided a minimum of RM500 is left in this Account. All remaining amount can be withdrawn when you reach 55 years old

With this EPF i-Saraan retirement fund scheme offered by our government to help the self-employed in retirement planning, if we compare it to bank’s fixed deposit of 2-3% at current economic situation, EPF annual dividend payout rate of minimum 2.5% and the additional 15% extra matching contribution offered by our government definitely stands out as a better deal.

For more information, please visit: https://www.kwsp.gov.my/ms/member/contribution/i-saraan

#EPF #retirementplan #retirementsaving #governmentbenefit #extramoney #dividend #interestreturn